Financial goals

Financial goals are big, personal goals you set for how you save and spend money. They can be things you hope to achieve in the short term or down the road. Either way, it’s often easier to achieve your goals if you’ve identified them beforehand. (If necessary, take a few steps back

It’s important to review your goals at least once a year to set expectations, chart your progress, and review your priorities. “Whenever something changes in your life or financial situation, it should be an indicator to review your goals.

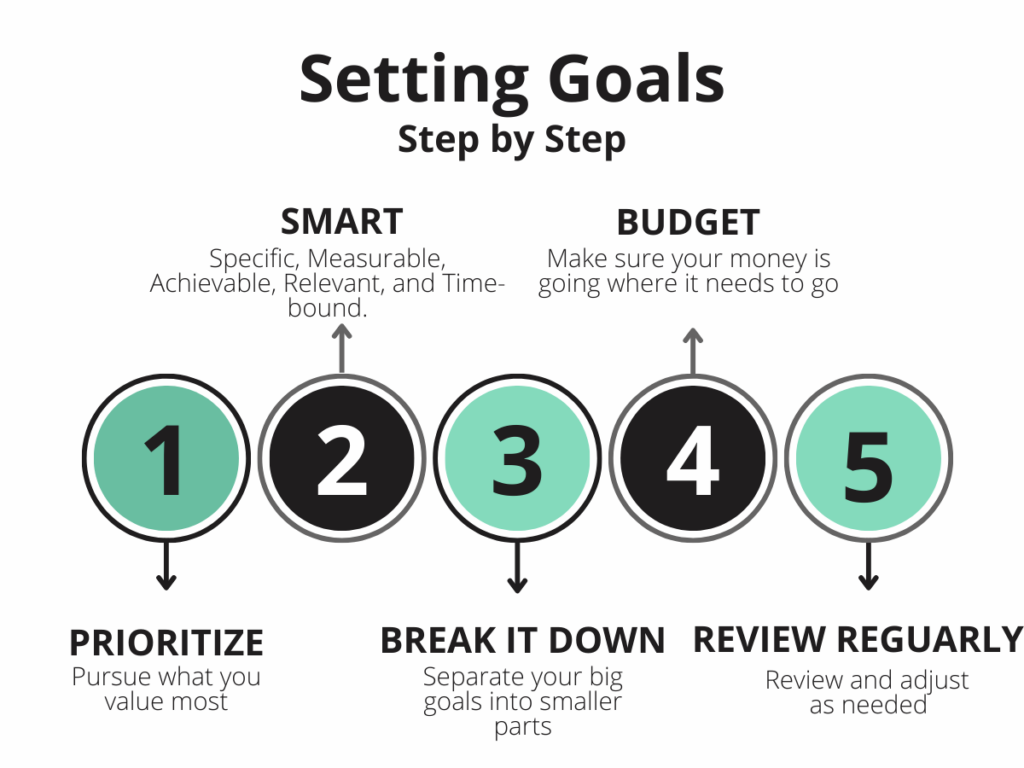

Reviewing and setting goals is an important part of financial planning. This allows you to ensure that your goals are realistic, relevant, and attainable, given your current financial situation and life circumstances. Here’s a step-by-step guide on how to review and set your goals.

-

Assess your current financial situation:

Start by taking a hard look at your current financial situation. This includes income, expenses, savings, investments, debts, and any major changes in your life (marriage, children, new job, etc.). Before setting or setting your goals, it is important to understand your financial situation.

Review your existing goals:

If you already have goals, review them to make sure they’re still relevant. Circumstances change and what was once a priority may no longer be. Be specific about what you want to achieve with each goal.

Prioritizing goals:

List your goals in order of importance. This will help you focus your efforts and resources on what is most important to you.

Smart goals:

Make sure your goals are specific, measurable, achievable, relevant, and time-bound (SMART). For example, instead of “save money,” make it “save $5,000 in a high-yield savings account by the end of next year.”Adjust for life changes, such as retirement, home ownership, or debt reduction.

Track progress:

Regularly monitor your progress toward your goals. This can be monthly or quarterly. This will help you stay on track and make adjustments as needed.

Seek professional advice:

If your financial situation is complicated, or if you’re not sure how best to achieve your goals, consult a financial advisor.

Stay flexible:

Remember that life is dynamic and circumstances may change. Be prepared to adjust your goals as needed. Flexibility is the key to successful financial planning.

Celebrating achievements:

When you reach a goal, take a moment to celebrate your success. Knowing your progress can motivate you to keep working toward your goals.

-

Importance of reviewing and adjusting

In short, reviewing and setting goals is an ongoing process that should be aligned with your current situation and life circumstances. This is an important part of staying financially healthy and achieving the financial future you want.

Reference:

https://www.google.com/search?q=review+and+adjust+financial+goals

Leave a Reply